Summary:

Digital transformation is helping insurance companies move away from slow, manual processes and adopt faster, more efficient ways of working. By using technologies like automation, data, and digital platforms, insurers can improve how they manage operations and interact with customers. It makes services quicker, more accurate, and more personalized, while also helping businesses reduce costs and make better decisions. As the industry continues to evolve, adopting digital approaches is becoming key to staying competitive and meeting modern customer expectations.

Why Insurance Businesses Are Going Digital

In today’s fast-moving world, insurance companies feel the pressure to keep up and evolve. Digital transformation in insurance isn’t just a trending topic; it’s become essential for staying relevant and ahead of the competition. As customer preferences shift toward quicker, digital-first experiences, traditional methods often slow, manual, and fragmented are simply not cutting it anymore. The emergence of digital-first insurers and insurtech players is ramping up competition, urging established companies to innovate. Plus, the urgency for efficiency which is vital for managing costs and improving turnaround times, can’t be ignored.

Technology is at the heart of this evolution, particularly with data, automation, and interconnected systems driving change. In this blog, we’ll dive into the benefits of digital transformation, key use cases, and the trends that are shaping the future of the insurance landscape.

What Is Digital Transformation in the Insurance Industry?

At its essence, digital transformation in the insurance industry involves reimagining operations through innovative technologies. It encompasses much more than merely digitizing processes; it represents a comprehensive business overhaul. Here’s what you need to know:

Definition

Digital transformation means investing in technology to redefine how insurance companies interact with customers and manage their internal operations.

Digitization vs transformation

While digitization focuses on converting manual tasks into digital formats, transformation involves a holistic change in business strategies and operational practices.

Key Areas for Transformation

Important areas for transformation include:

- Operations: Streamlining workflows to boost efficiency.

- Customer Experience: Providing seamless, personalized services.

- Data Management: Utilizing data for instant insights.

- Distribution Channels: Enhancing points of contact with customers.

Process changes

Incorporating automation, integration, and real-time workflows can greatly improve service delivery and responsiveness.

Customer impact

The aim is to create smooth journeys where insurance offerings are aligned with individual customer needs.

Business impact

Implementing these changes fosters efficiency, agility, and growth, allowing firms to quickly adapt to market changes.

What Is Driving Digital Transformation in Insurance Services

Several factors are prompting insurance firms to embrace digital transformation:

- Demand for Faster Experiences: Customers want quick, self-service options when dealing with their insurers.

- Competition from Digital Players: The rise of digital-first insurers is pushing traditional companies to upgrade their systems.

- Cost Efficiency Pressures: With increasing costs, efficient operations are critical for maintaining profitability.

- Data and Analytics: More data leads to deeper insights, enabling personalized offerings and better decision-making.

- Regulatory Compliance: Digital solutions can help ease the challenges of meeting compliance requirements.

How Digital Transformation Works in the Insurance Industry

Successfully implementing digital transformation relies on several operational components:

1. Unified Data Access: Having a centralized source of truth across various systems is vital for consistency.

2. Workflow Automation: Streamlining processes like claims management and underwriting accelerates response times.

3. Digital Platforms: Apps, portals, and dashboards improve customer engagement and support.

4. Real-Time Data Usage: Ongoing access to insights leads to quicker, data-informed decisions.

5. Continuous Improvement: Leveraging analytics creates a culture of ongoing growth and adaptation.

6. Third- Party Integrations: APIs and partnerships expand capabilities and foster innovation.

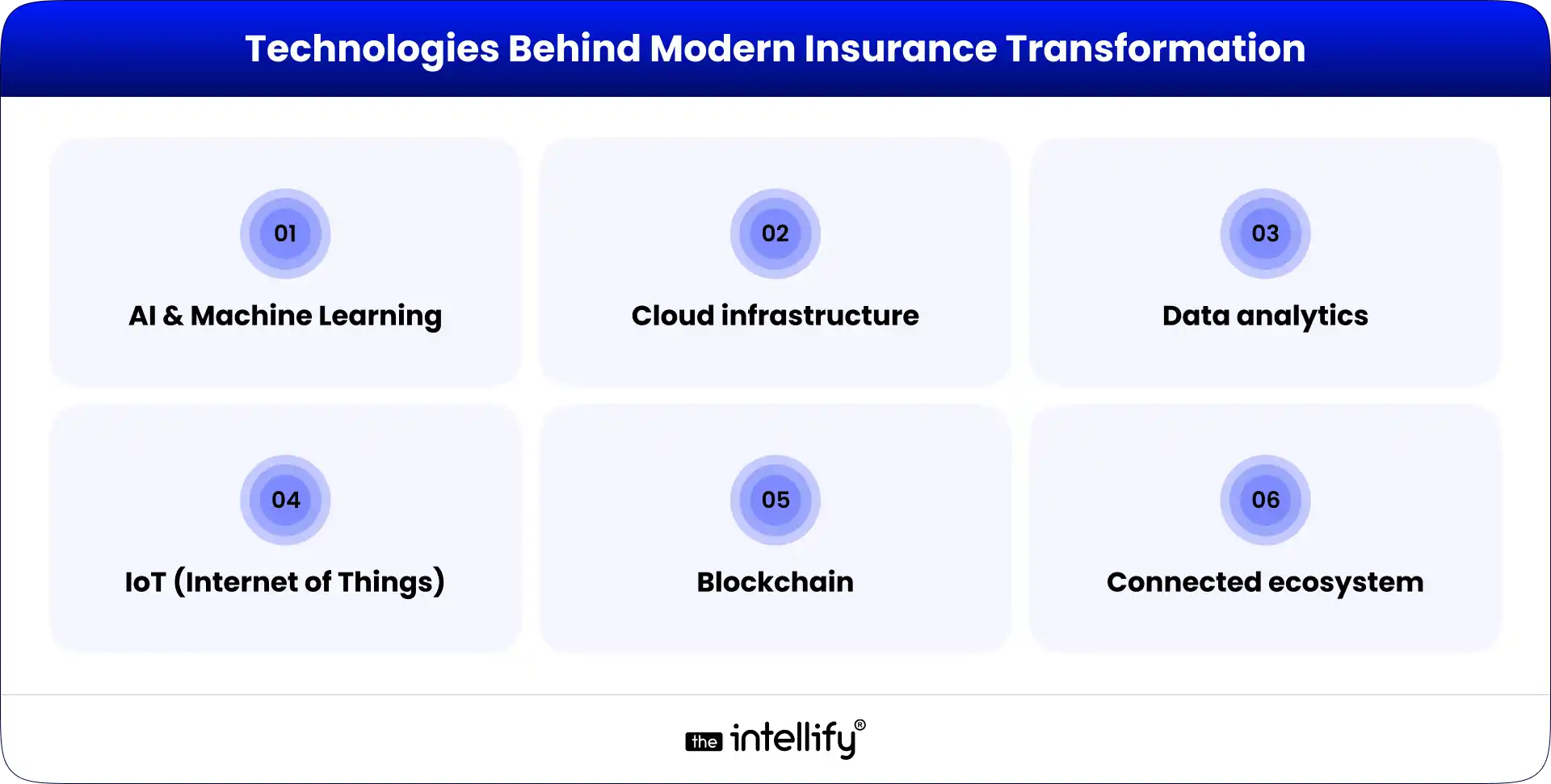

Technologies Behind Modern Insurance Transformation

A few key technologies are paving the way for digital change in insurance:

- AI & Machine Learning: Enhancing operations, improving risk assessments, and spotting fraud.

- Cloud infrastructure: Providing scalability and flexibility for a variety of applications.

- Data analytics: Offering actionable insights for improved personalization and customer experiences.

- IoT(Internet of Things): Supporting real-time and usage-based insurance models.

- Blockchain: Ensuring secure and transparent transactions.

Key Benefits of Digital Transformation in Insurance Sector

Digital transformation offers numerous advantages, such as:

- Faster processes: Reducing manual tasks speeds up operational efficiency.

- Improved customer experience: Personalized interactions and quicker service boost satisfaction.

- Better Risk Assessment: Reliable data allows for more informed underwriting decisions.

- Cost efficiency: Streamlined processes yield significant operational savings.

- Enhanced Fraud Detection: Advanced algorithms improve monitoring and compliance.

- Accelerated Product Development: Integrated systems facilitate rapid innovation.

Where Digital Transformation Delivers Value

Digital transformation has a direct impact on various stages of the insurance value chain:

- Customer Onboarding: Simplifying policy purchases creates a seamless entry for customers.

- Claims processing: Automation expedites claims handling and resolution.

- Customer support: Digital channels enhance engagement and quicken responsiveness.

- Underwriting and pricing: Efficient data analysis provides the ability for real-time decision-making.

- Agent and Broker Enablement: Empowered agents can offer better service with enhanced tools.

Real-World Use Cases Across the Insurance Value Chain

Let’s explore some compelling examples that highlight the effectiveness of digital transformation:

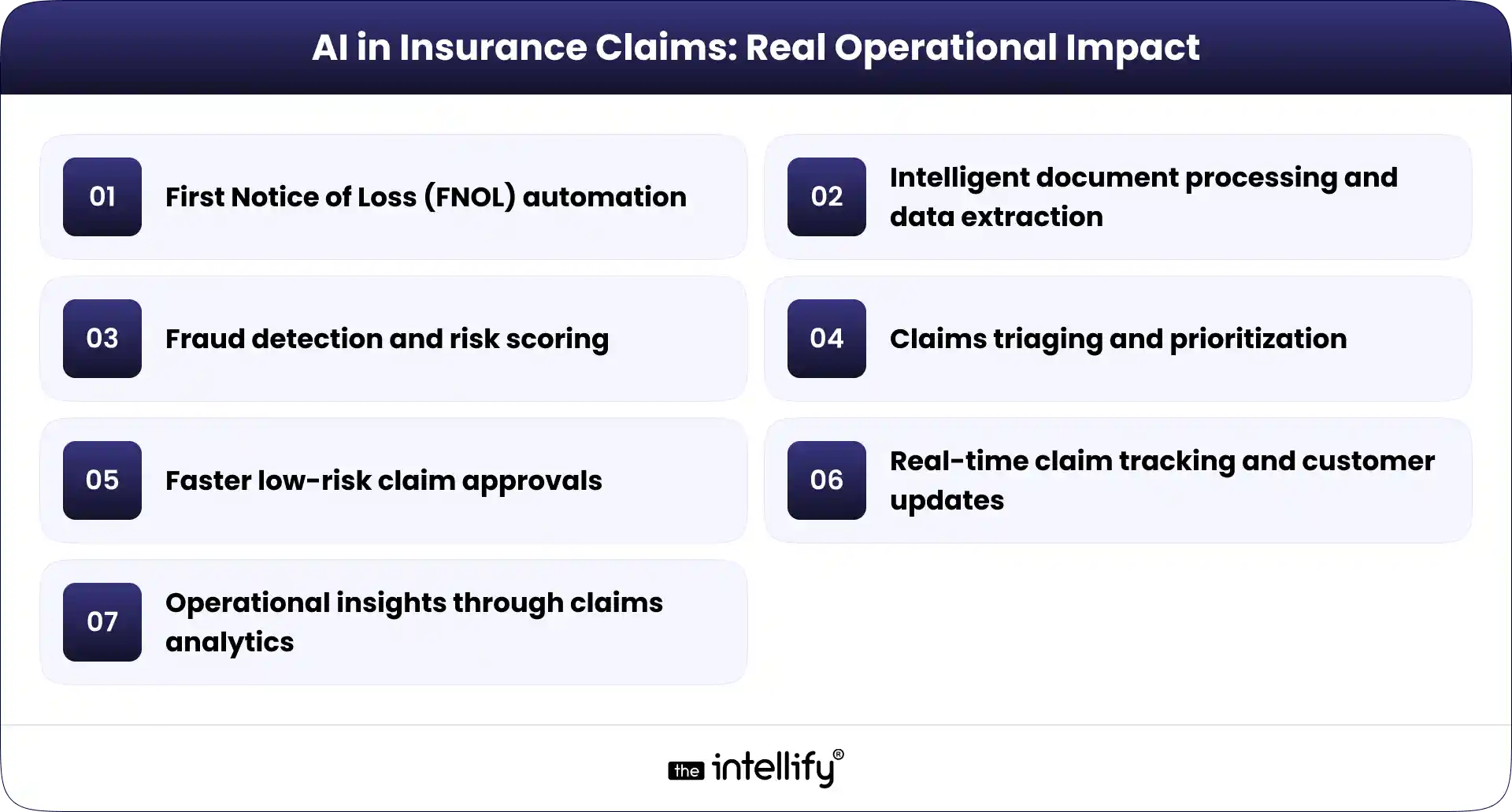

Claims & Operations

Automated claims processing: Reduces processing times while improving accuracy.

Fraud detection systems: Utilizing machine learning to identify irregularities.

Document verification: Streamlining the submission process for users.

Customer Experience

Chatbots and virtual assistants: Offering 24/7 support for customer questions.

Self-service portals: Allowing customers to manage their policies and claims independently.

Faster onboarding journeys: Minimizing wait times and simplifying the policy initiation process.

Product Innovation

Telematics-based insurance: Implementing usage-based pricing models based on driving behavior.

Personalized policy recommendations: Crafting options tailored to individual profiles.

Usage-based insurance models: Setting premiums based on actual usage rather than generalized estimates.

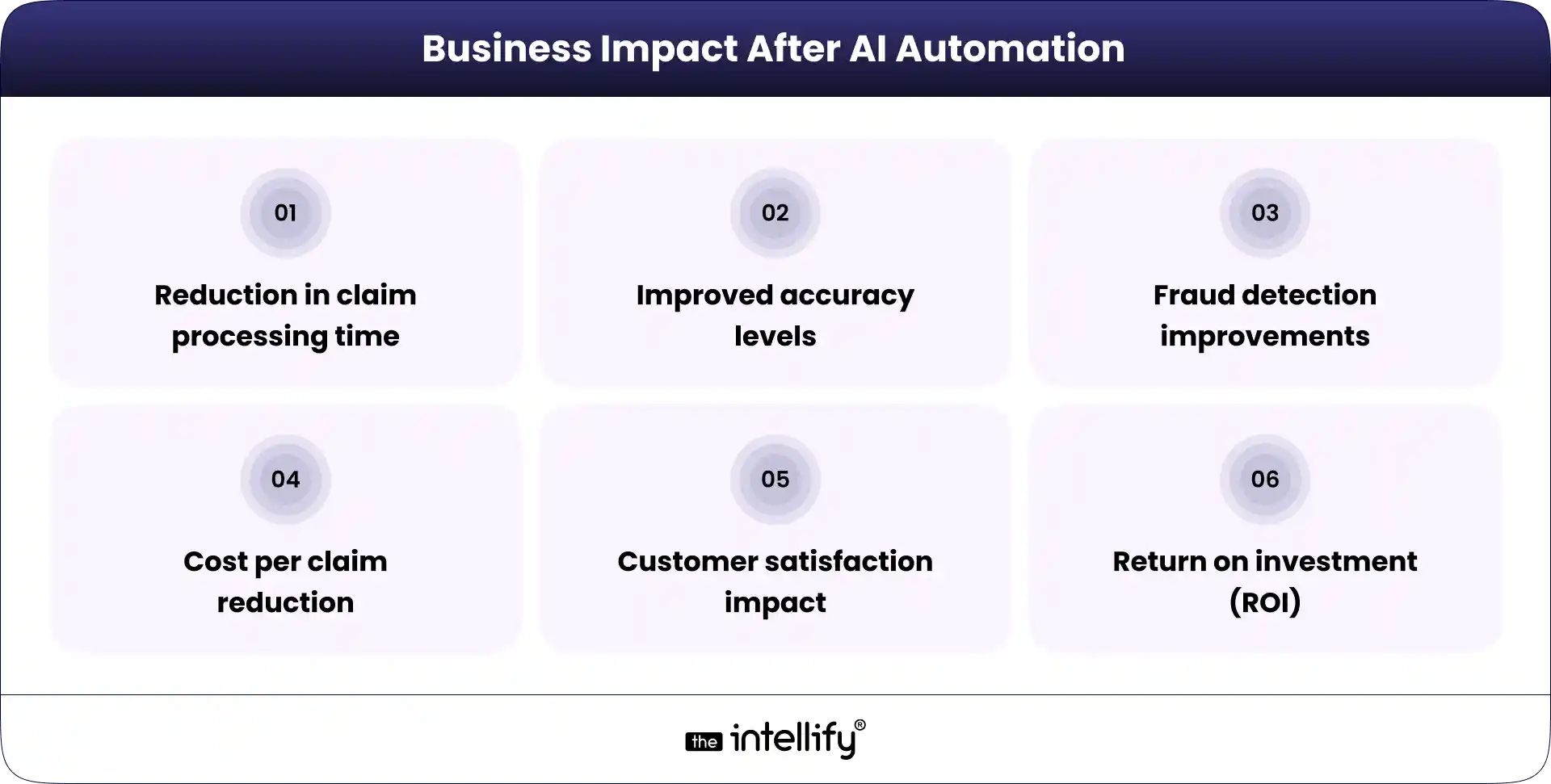

Business Impact of Digital Transformation for Insurance Companies

The outcomes of digital transformation are notable:

- Reduced operational costs: Greater efficiency leads to lower expenses.

- Faster turnaround times: Quick service enhances customer satisfaction.

- Higher customer retention: Happy customers are more likely to remain loyal.

- New revenue opportunities: Innovations can pave the way for fresh business models and offerings.

- Data-driven decision-making: Leveraging data facilitates informed planning and strategies.

Challenges Insurance Companies Face During Digital Adoption

Even with the many benefits, insurance companies face a range of challenges during their digital journey:

- Legacy system: Older technology can resist integration, complicating progress.

- Data privacy and security risks: Safeguarding customer data is paramount.

- Resistance to change: Some employees might be hesitant to adapt, slowing transformation efforts.

- High initial investment: The upfront costs of new technologies can feel overwhelming.

- Compliance complexity: Navigating regulatory requirements can be daunting.

How to Implement Digital Transformation in Insurance

Implementing a successful digital transformation strategy involves more than just adopting new tools. Insurance companies need the right partner with expertise in digital transformation and insurance development services to ensure smooth implementation and long-term success. Key factors to consider include:

- Clear roadmap and priorities: Setting a structured approach to your transformation journey.

- Customer-first approach: Keeping customer needs and expectations at the forefront throughout the process.

- Scalable technology: Opting for solutions that can grow alongside your business.

- Team upskilling: Equipping staff with the necessary skills for thriving in a digital world.

- Strategic partnerships: Collaborating with tech providers for expertise and innovative solutions.

Emerging Trends Shaping the Future of Insurance

The insurance industry is moving toward thrilling opportunities:

1. AI-driven Predictive Insurance: Using data to anticipate and prepare for future claims.

2. Hyper-personalized policies: Custom offerings grounded in thorough customer insights.

3. Embedded insurance models: Seamlessly integrating insurance into established customer journeys.

4. Fully digital insurance platforms: Facilitating all interactions online for maximum convenience.

5. Real-time data usage: Utilizing data from IoT devices to dynamically adjust policies.

Conclusion:

To sum it up, digital transformation in the insurance industry isn’t just about technology, it’s about rethinking how businesses connect with customers while optimizing operations. Early adaptation is vital to capitalizing on digital opportunities, as it dramatically affects long-term success and competitiveness.

By embracing digital transformation, insurance companies can elevate customer satisfaction, streamline workflows, and position themselves for future growth. The path to innovation starts now let’s seize the opportunities that lie ahead!

Frequently asked questions

1. Why are insurance companies focusing more on digital transformation now?

Customers today expect quick responses, online access, and smooth experiences. Traditional systems struggle to keep up with this, so insurers are moving towards digital solutions to stay competitive and meet these expectations.

2. How does digital transformation make insurance processes faster?

It reduces manual work by automating tasks like claims handling, underwriting, and approvals. This not only speeds up operations but also reduces delays and improves overall efficiency.

3. Can digital transformation improve the claims process?

Yes, it makes claims faster and more transparent. Customers can submit and track claims online, while automation helps insurers process them quickly with fewer errors.

4. What role do mobile apps play in digital transformation in insurance?

Mobile apps give customers easy access to services like buying policies, renewing plans, or filing claims. They make the entire experience more convenient and accessible anytime, anywhere.

5. Can traditional insurance companies adapt to digital transformation?

Yes, many companies start small by digitizing specific processes like claims or customer support. Over time, they gradually expand and build a more complete digital system.

6. Does digital transformation help in reducing fraud in insurance?

Yes, advanced technologies can detect unusual patterns and flag suspicious activities early. This helps insurers prevent fraud and improve security.

7. How does digital transformation improve customer experience in insurance?

It makes services faster, simpler, and more personalized. Customers can interact easily, get quick responses, and access everything online without unnecessary delays.